Running a business in Dubai is exciting. But it’s also challenging when it comes to managing money. Good accounting makes this much easier. Let’s explore how it can help you make smarter financial decisions. Why Dubai Is Different Dubai’s business world is special. You’ve got free zones, new tax rules, and lots of opportunities. But these opportunities come with their own money challenges. That’s why local businesses need a solid financial plan. How Accounting Makes Budgeting Easier Think of accounting like a GPS for your money. It shows you: Where your money is coming from Where it’s going How much you’re really spending How much you’re earning This clear picture helps you make better plans for your business. Real Benefits You Can See Better Money Forecasting Good accounting helps you: Know when busy seasons are coming Set goals you can reach Understand how customers spend Get ready for market changes Smarter Spending With proper accounting, you can: Spot where you’re spending too much Find ways to cut costs See spending patterns clearly Make your profits bigger Better Cash Flow Understanding your money flow helps you: Keep enough cash on hand Plan for regular bills Manage your inventory costs Prepare for surprise expenses Handling Dubai’s Tax Rules Recent tax changes in Dubai mean you need to: Plan for VAT payments Get ready for corporate tax Use available tax benefits Follow local rules Making Smart Business Moves Good accounting records help you decide: When to grow your business What equipment to buy When to hire people Which markets to enter Using Modern Tools Today’s accounting software gives you: Real-time expense tracking Automatic reports Budget comparisons Quick financial insights Getting Professional Help Working with accounting experts gives you: Knowledge of Dubai’s rules Smart financial planning Help staying compliant Growth strategies Best Ways to Budget in Dubai Regular Checkups Keep your budget healthy by: Checking it every month Updating your plans as needed Learning from past months Setting new goals Good Record Keeping Always keep track of: Daily business activity Decision-making info Legal requirements Future budget plans Special Tips for Different Businesses Retail Stores Focus on: Stock costs Seasonal planning Staff schedules Marketing costs Service Companies Watch your: Project costs Employee time use Running costs Customer getting costs Manufacturing Keep track of: Material costs Equipment care Production timing Quality checks Common Challenges and Solutions Understanding Dubai’s Market Watch for: Market changes Seasonal effects Competition Local business customs Growing Your Business Plan for: Growth costs New market entry Staff needs Building needs How Elite Auditing Helps We offer: Deep financial review Budget planning Rule compliance help Expert accounting Taking Action Ready to make your business finances better? Here’s how to start: Book a meeting with us Review your current system Make an improvement plan Put new systems in place Also Read: What Are The Benefits Of Outsourcing Accounting In UAE? FAQs Why do I need professional accounting for my Dubai business? Think of professional accounting as your business’s financial guardian. It helps you: Follow UAE rules without headaches See your money picture clearly Make smarter business choices Keep your business running smoothly How often should I look at my budget? We suggest: Monthly check-ins to see how you’re doing Deeper reviews every three months Extra checks when business is growing fast Quick reviews when market conditions change What can Elite Auditing do for my business? We handle everything your business needs: Monthly money reports Budget planning and tracking Cash flow help Tax planning Financial analysis Business advice VAT services Corporate tax help How do you help with taxes? We make taxes simpler by: Finding legal ways to save money Planning for tax payments Keeping up with new rules Making sure you follow UAE laws What’s the difference about bookkeeping and professional accounting? Think of it this way: Bookkeeping is like taking daily notes Professional accounting is like having a financial advisor who: Analyzes your money patterns Plans for your future Helps you make smart tax choices Guides your business decisions How do I know if my budget system works? A good budget should: Correctly predict your monthly money in and out Keep cash flowing smoothly Help your business grow Show you how you’re doing Help you make good choices What records do I need to keep? Keep track of: Daily money movements Bank statements Sales and purchase papers Expense receipts Staff payments Business property lists VAT records Yearly financial reports How can accounting help my business grows? Good accounting: Shows where you can grow Finds money you need Spots growth chances Keeps cash flowing Measures investment returns Helps get loans Tracks how you’re doing Why use accounting software? New accounting tools give you: Real-time money tracking Automatic reports Accurate cash flow views Better expense control Easier tax work Time savings Better data protection What’s special about Dubai accounting? Dubai businesses need special attention to: UAE VAT rules Free zone regulations Corporate tax planning International money handling Multiple currency tracking Local business rules Cultural business practices Can you help new and established businesses? Yes! We help: New businesses set up strong systems Growing businesses get better Established businesses stay successful What should I look for in an accounting service? Choose someone with: UAE rule knowledge Business experience Professional training Full service options Modern technology Good client feedback Clear communication Quick responses How can I improve my cash flow? Better accounting helps by: Watching payment timing Managing customer payments Controlling costs Planning for bills Spotting money patterns Preventing shortages Making the most of your working money What budget mistakes should I avoid? Watch out for: Guessing at expenses Missing seasonal changes Not saving for emergencies Poor cash planning Ignoring market changes Messy record keeping Not checking your budget enough Related: Why Accounting Services Matter for Your Small Business in Dubai, UAE

Getting your taxes set up in the UAE doesn’t have to be confusing. Whether you’re starting a business or already running one, this guide will walk you through the process step by step. The Basics of UAE Taxes The UAE is known for being tax-friendly. You don’t pay tax on your personal income here. But since 2018, businesses need to pay something called VAT (Value Added Tax). The Federal Tax Authority, or FTA for short, handles all tax matters. Do You Need to Register? It’s simple – if your business makes more than AED 375,000 a year, you must register for tax. If you make between AED 187,500 and AED 375,000, you can choose to register if you want to. Many businesses find it helpful to register even when they don’t have to. How to Register: A Simple Guide 1. Get Your Papers Ready Before you start, gather these items: Your trade license Passports of all owners and managers Emirates ID (if you live in the UAE) Your business bank account information A recent power or water bill from your business location Papers that show you own the business 2. Set Up Your FTA Account Go to the tax authority’s website and sign up. You’ll need: An email address you use regularly Your phone number Basic information about your business They’ll send you an email to confirm everything works. 3. Fill Out the Registration Form Now you’ll need to enter: What your business does Your money details Information about everyone who owns part of the business Your bank details Take your time with this part. It’s better to get it right the first time. 4. Send in Your Documents Put all your papers into the FTA website. Remember: Make sure everything is easy to read Use PDF files when you can Don’t send files that are too big Give each file a clear name Also Read: How to Prepare for UAE Corporate Tax Audits 5. Pay Any Fees Most basic registrations are free. If you need to pay anything, keep your receipt safe. 6. Wait to Hear Back The tax office usually takes about 20 working days to check everything. They might ask you for more information during this time. What Happens After You Register? You’ll get: A tax number (called a TRN) A certificate saying you’re registered A way to log in to the tax website Keep these safe – you’ll need them to: Send in your tax forms Make proper tax receipts Talk to the tax office Keeping Up With Your Taxes To stay on the right side of the law: Send in your tax forms on time Keep good records of everything Tell the tax office if anything about your business changes Follow all the tax rules Special Cases Worth Knowing About If You’re in a Free Zone Free zone companies work a bit differently. You might need: Different papers Special steps to register Different tax rules For Small Business Owners If you run a small business, think about: Whether registering early might help you How to keep track of your money If you need help from an expert For Companies From Other Countries If your company isn’t from the UAE, you’ll also need: Papers showing you’re registered in your home country Documents with special stamps (called apostilles) Official translations of your papers Common Mistakes to Watch Out For Save yourself trouble by avoiding these mix-ups: Waiting too long to register Not sending in all your papers Getting your numbers wrong Not keeping good records Sending in tax forms late When to Get Help Think about getting professional help if: Your business is complicated You’re not sure about the rules You want to make sure you’re doing everything right You work in multiple countries Conclusion Getting registered for tax in the UAE isn’t as hard as it might seem. If you follow these steps and keep good records, you’ll be fine. Just remember to: Start early Stay organized Keep good records Ask for help if you need it While this guide gives you the main points, tax rules can change. When in doubt, check with the tax office or talk to a tax expert. They’ll have the latest information to help you do things right. FAQs How long does it take to get registered? Usually 15-20 working days, if you have all your papers ready. Can I register without a business license? No – you need a valid license first. What if I don't register when I should? You could get fined up to AED 20,000 and have trouble with your business. Can I cancel my registration? Yes, if your business stops or gets smaller. Just tell the tax office through their website. Do new businesses need to register right away? If you think you’ll make more than AED 375,000 in your first month, yes.

Hello! We’re Elite Auditing, your friendly tax experts in Dubai. Let’s talk about VAT penalties in simple terms. Think of VAT like a receipt-keeping game – play by the rules, and you’re fine. Break the rules, and it costs you money. Why Should You Care About VAT Rules? Back in 2018, the UAE started charging VAT on most things we buy and sell. It’s like a small fee that helps build roads, schools, and hospitals. When businesses don’t handle VAT correctly, they have to pay extra money as penalties. What Happens If You Break VAT Rules? Missing the Registration Deadline Think of VAT registration like getting a driver’s license – you need it before you can drive a car. If you don’t register: Late Tax Returns Imagine turning in your homework late – teachers don’t like it, and neither does the tax office: Late Payments The tax office wants its money on time. If you’re late: Wrong Information on Tax Forms Making mistakes on your VAT forms is like getting your math wrong: Why Do Businesses Get These Penalties? Bad Bookkeeping Many businesses get in trouble because they’re messy with paperwork. Keep these for 5 years: Not Understanding the Rules VAT can be tricky. People often get confused about: Computer Problems Sometimes technology lets us down: How to Stay Out of Trouble 1. Get Organized 2. Train Your Team Make sure everyone knows: 3. Use Good Software Get a computer program that: 4. Check Your Work Make it a habit to: What to Do If You Get a Penalty First Steps Fix the Problem How Elite Auditing Makes Your Life Easier We’re like your VAT buddy in Dubai. We help you: Smart Tips to Stay Safe Keep Track of Time Keep Good Records Get Expert Help Conclusion Don’t let VAT scare you! With good habits and the right help, you can avoid penalties and keep your business healthy. Elite Auditing is here to make VAT easy for you. Need a friend to help with VAT? Give us a call at Elite Auditing. We speak your language and make tax stuff simple! FAQs When do I need to register for VAT? If your business makes more than AED 375,000 in a year, you have 30 days to register. Can I argue against a penalty? Yes! You have 20 working days to explain why you think the penalty is wrong. What if I can't pay my penalties? Talk to the tax office – sometimes they let you pay bit by bit, but don’t wait too long. How often do I need to file VAT returns? Usually every three months, but some businesses do it monthly or yearly. Can they reduce my penalties? Sometimes, if you have a really good reason, but don’t count on it.

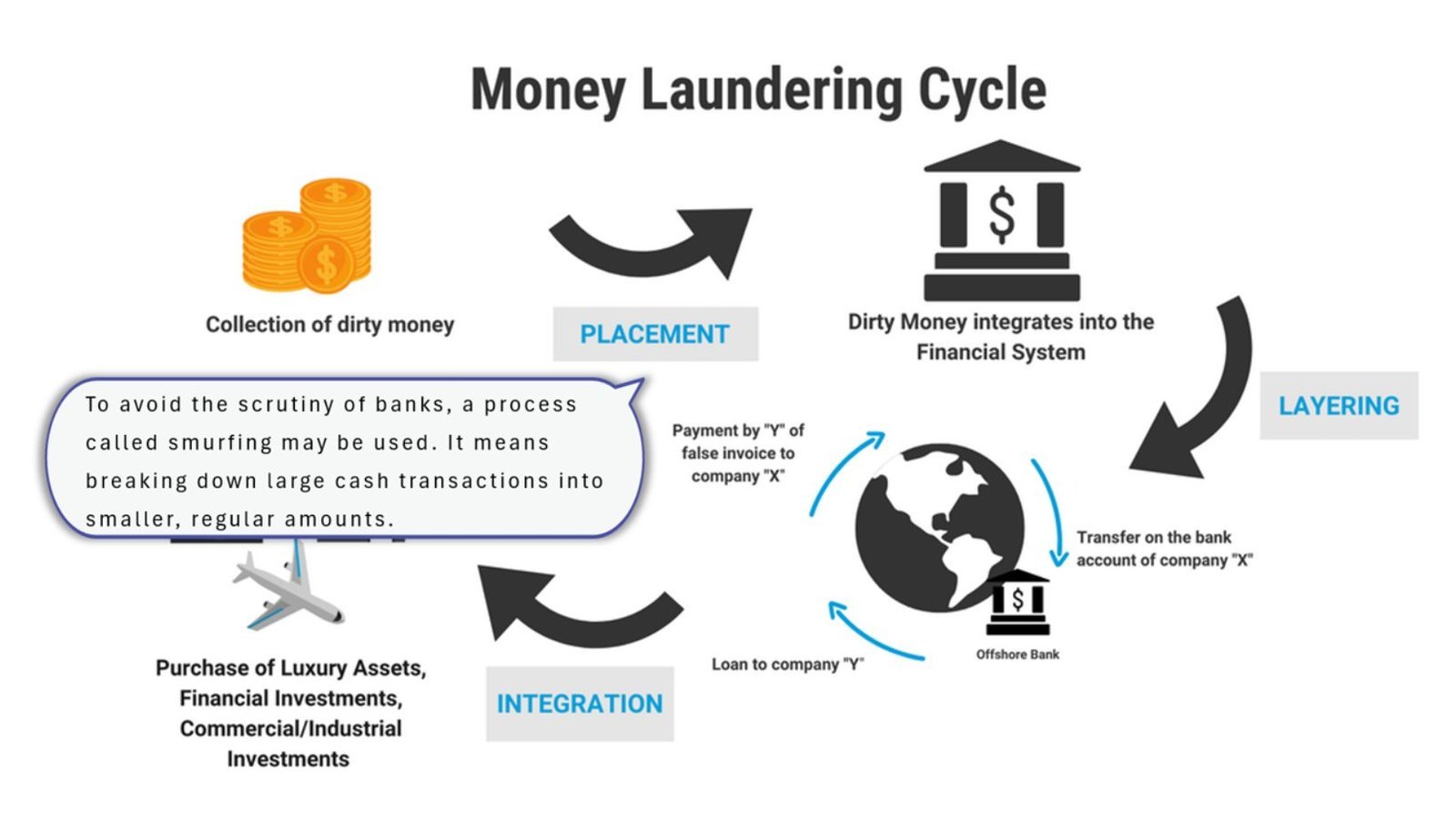

Money laundering is when criminals hide illegal money and make it look legal. It is harmful to businesses, the economy, and society. At Elite Auditing, we help businesses in Dubai understand and fight money laundering. In this article, we explain the three stages of money laundering and how to stop it in easy terms. What Is Money Laundering? Money laundering happens when money earned from crimes is made to look like it came from a legal source. Criminals use this process to avoid getting caught. Why Is It Dangerous? It supports illegal activities like fraud or corruption. It damages businesses and economies. It can lead to fines or penalties for companies that unknowingly help. Money laundering is done in three steps: Placement Layering Integration Step 1: Placement What Happens in Placement? This is the first stage of money laundering. Here, criminals put illegal money (often in cash) into the financial system. For example, they might deposit it into a bank account or buy expensive items. Common Techniques Depositing Small Amounts: Criminals deposit money in small chunks to avoid suspicion. Buying Valuables: They purchase things like gold, jewelry, or cars to later sell for clean money. Fake Businesses: Setting up a company to explain where the cash came from. Risks for Businesses Banks, real estate agents, and other businesses dealing with cash are at risk. If they don’t follow rules, they may unknowingly help launder money. How to Stop It Know Your Customers: Verify customer identities and understand their transactions. Spot Unusual Deposits: Watch out for large cash deposits with no clear reason. Train Employees: Teach staff how to detect suspicious behavior. Step 2: Layering What Happens in Layering? This is the second step. Here, criminals move the money around to hide its illegal source. They use many transactions to confuse investigators. Common Techniques Transferring Funds: Moving money between different accounts or countries. Shell Companies: Setting up fake companies to hold or move money. Buying and Selling Assets: Using the money to buy things like stocks, then selling them to mix the funds. ExampleIn the Danske Bank Scandal, criminals transferred illegal money between several accounts to make it hard to trace. Risks for Banks and Businesses Financial institutions are at risk during this stage. Without proper controls, criminals can use their systems to hide money. How to Stop It Monitor Transactions: Use software to flag unusual or frequent transfers. Extra Checks for High-Risk Areas: Investigate transactions involving high-risk regions. Work with Law Enforcement: Share suspicious data with authorities when needed. Step 3: Integration What Happens in Integration? This is the final step. The illegal money is now part of the legal economy. It is used for investments, purchases, or luxury items without drawing attention. Common Techniques Buying Property: Criminals use the money to buy real estate. Investing in Businesses: They invest in legitimate companies to earn clean profits. Luxury Spending: Using the money to buy yachts, cars, or designer goods. Risks for the Economy Once the money is integrated, it looks legal. Criminals gain financial power, which they can use to fund more crimes. How to Stop It Check Large Purchases: Review high-value transactions carefully. Follow Strict Rules: Enforce anti-money laundering laws in real estate and other industries. Encourage Reporting: Make it easy for employees to report suspicious actions. How to Fight Money Laundering What Governments Can Do Enforce AML Laws: Governments should create strong laws to prevent money laundering. Support Law Enforcement: Provide tools and resources to catch criminals. Work with Other Countries: Money laundering often crosses borders, so global cooperation is essential. What Businesses Can Do Follow Compliance Rules: Set up systems to check and report suspicious transactions. Hire Experts: Work with companies like Elite Auditing for AML solutions. Report Red Flags: Always report anything suspicious to the proper authorities. How to Protect Your Business Understand Risks Identify where your business might be exposed to money laundering, especially if you handle cash or high-value goods. Stay Updated on Laws Money laundering laws can change. Make sure your company knows the latest regulations. Use Technology Invest in tools that detect suspicious transactions. Train Your Team Employees should know how to spot and stop suspicious activities. Conduct Regular Audits Regular checks can help you catch and fix issues early. Conclusion Money laundering is a global problem, but we can stop it by understanding its three stages: placement, layering, and integration. By following AML rules, training employees, and working with experts like Elite Auditing, businesses can protect themselves and the economy. Stopping money laundering isn’t just about following laws—it’s about creating a safe, fair, and honest system for everyone. FAQs About Money Laundering How Can Companies Protect Themselves? • Always verify customer details. • Watch out for unusual transactions. • Train employees to identify and report red flags. What Is the Role of AML Officers? AML (Anti-Money Laundering) officers ensure businesses follow the rules. They monitor activities, report suspicious cases, and prevent money laundering. What Happens If a Business Breaks AML Rules? Breaking AML laws can result in: • Fines or penalties. • Loss of business reputation. • Legal actions or business closure. Why Do Criminals Use Fake Companies? Fake companies (shell companies) make illegal money look clean. These companies have no real operations but are used to move or hide money.

The UAE is a top business destination, known for its growing economy and opportunities. If you own or manage a business here, you need to prepare your financial statements correctly. But what rules should you follow? This article explains everything you need to know about the accounting standards required in the UAE. It’s written in simple terms to make it easy for everyone to understand. What Are Accounting Standards? Accounting standards are the rules businesses use to create their financial statements. These rules make sure the numbers are accurate, fair, and easy to compare. Why Are They Important? They give a clear picture of a company’s finances. They help investors, banks, and others make decisions. They make sure businesses follow fair practices. Accounting Standards in the UAE Which Standards Are Used? The UAE uses International Financial Reporting Standards (IFRS). These are global rules that help businesses prepare their financial reports in a way that everyone can understand. Main Features of IFRS Fair and Clear ReportingIFRS makes sure businesses show their financial position clearly. Four Key Financial StatementsBusinesses following IFRS must prepare: A balance sheet, which lists what the company owns (assets) and owes (liabilities). An income statement, which shows profits or losses. A cash flow statement, which tracks money coming in and out. A statement of changes in equity, which explains changes in shareholder investments. TransparencyIFRS requires businesses to share detailed information. This includes the methods used to prepare the numbers and any special decisions management made. Who Needs to Follow IFRS? Applicable Companies Most companies in the UAE must follow IFRS, including: Public Companies: Companies listed on stock markets like Nasdaq Dubai. Large Private Companies: Big businesses with international clients or investors. Banks and Financial Institutions: Entities regulated by the UAE Central Bank. Small Businesses Small and medium enterprises (SMEs) may follow simpler standards. However, if they deal with international partners or investors, they might also need to follow IFRS. Read More: Is It Worth Paying for a Financial Advisor in Dubai? Steps to Prepare Financial Statements with IFRS Keep Records Organized Make sure all transactions are recorded properly. Using accounting software or hiring experts like Elite Auditing can help. Follow the Framework Use the IFRS conceptual framework as your guide. It explains how to: Record assets and liabilities. Measure profits and losses. Present financial reports clearly. Prepare the Required Reports For example, your balance sheet should include: Assets: Like cash, buildings, and equipment. Liabilities: Such as loans or unpaid bills. Equity: The money invested by owners or shareholders. Add Necessary Details IFRS requires extra notes in your financial statements. These notes explain: Accounting methods you used. Important decisions or changes in your business. 5. Audit Your Reports Get an expert, like Elite Auditing, to check your reports. This ensures everything is correct and complies with the law. Benefits of Using IFRS Clear Financial Information: Investors and stakeholders can trust your reports. Global Recognition: IFRS makes it easier to work with international partners. Better Decisions: With accurate data, management can make smarter business choices. Legal Compliance: Following IFRS helps you meet UAE regulations. Tips for Businesses in Dubai Stay Updated: Keep track of IFRS updates. Train Staff: Ensure your team understands IFRS rules. Work with Experts: Firms like Elite Auditing can guide you. Use Technology: Choose accounting tools that follow IFRS standards. Plan Audits: Regular audits can catch and fix mistakes early. Conclusion In the UAE, businesses must prepare their financial statements using IFRS standards. These rules ensure transparency, accuracy, and compliance with local laws. Whether you’re running a small business or a large corporation, following IFRS helps you stay competitive and trustworthy. If you need help, reach out to Elite Auditing. Our team provides expert guidance to keep your financial reporting compliant and reliable. By following the right standards, you can build trust and success in the UAE market. FAQs About UAE Accounting Standards What Happens if a Company Doesn’t Follow IFRS? Not following IFRS can lead to: • Legal fines or penalties. • Losing investor trust. • Problems with regulators or banks. How Do IFRS Rules Change? The rules are updated by the IFRS Foundation. Businesses must keep up with changes to stay compliant. Can UAE Companies Use Other Standards? Some foreign companies operating in the UAE may use their home country’s standards. However, they still need to align with IFRS for reporting in the UAE. How Does IFRS Impact Taxes? IFRS makes it easier to calculate profits accurately. This is helpful for paying corporate taxes under UAE laws.

Businesses in the UAE need to follow corporate tax laws carefully to avoid problems and save money. One important rule is the Qualifying Group Relief. This allows companies in the same group to transfer assets and liabilities without immediately paying taxes. However, if certain conditions aren’t met, the Federal Tax Authority (FTA) can take back the tax relief through a process called clawback. This guide, brought to you by Elite Auditing, will explain clawback in simple terms so you can stay informed and avoid issues. What Is Qualifying Group Relief? Qualifying Group Relief lets companies in the same group transfer assets and liabilities to each other without paying taxes right away. It helps businesses restructure or simplify ownership without financial penalties. For example, a company can move machinery to another group company for business purposes without worrying about taxes on the transfer. What Is a Clawback? A clawback happens when the tax relief is reversed because the conditions for the relief weren’t followed. The FTA then asks the company to pay the taxes they avoided earlier. Simple Terms to Know Here are some important terms you’ll read about: Transferor: The company giving the asset or liability. Transferee: The company receiving the asset or liability. Qualifying Group: A group of businesses under common ownership that meet specific conditions. Tax-Neutral: A transfer with no immediate tax. FTA: Federal Tax Authority, which enforces tax laws in the UAE. Rules for Qualifying Group Relief To qualify for tax relief, companies must meet these rules: Both companies (transferor and transferee) must be in the same qualifying group. The transfer must not cause big changes in who owns the assets or liabilities. The transaction must follow all UAE Corporate Tax Law rules. What Causes a Clawback? The FTA can claw back the tax relief if any of these things happen: 1. Asset Is Transferred Again If the transferee sells or transfers the asset outside the group within two years, the relief is revoked. Example: Company A transfer’s machinery to Company B under the relief. Company B sells the machinery to an outside company within two years. The FTA applies a clawback, and Company A must pay taxes on the original transfer. 2. Leaving the Group If either the transferor or transferee leaves the qualifying group within two years, the clawback applies. This can happen due to: A change in ownership. A company becoming a free zone person or exempt person. 3. Mismatched Financial Years If group members don’t align their financial years, it may trigger a clawback. Example: Company A and Company B align their financial reporting initially. In year two, Company B changes its financial year and no longer matches the rest of the group. The clawback can be triggered. 4. Shares Are Transferred Shares issued as part of a business restructuring may trigger a clawback if they are transferred outside the qualifying group. Also read: Determining the Taxable Income for an Unincorporated Partnership What Happens When a Clawback Is Triggered? For the Transferor The company giving the asset (transferor) must calculate the gain or loss from the original transfer and include it in their taxable income. For the Transferee The company receiving the asset (transferee) must adjust its financial records. This includes updating depreciation or amortization for tax purposes. Additional Costs Companies may face extra tax bills, penalties, or compliance fees. How to Avoid a Clawback Here are simple tips to stay safe: Keep Everyone in the Group Make sure both the transferor and transferee stay in the qualifying group for at least two years. Watch Ownership Changes Avoid major ownership changes that could make the group ineligible. Align Financial Years Ensure all group members use the same financial year. Get Expert Help Hire experienced tax consultants like Elite Auditing to guide you through compliance. Why Choose Elite Auditing? Understanding corporate tax laws can be tricky, but you don’t have to do it alone. Elite Auditing can help your business with: Tax compliance to meet FTA rules. Expert advice on group restructuring. Detailed corporate tax guides for your company. With our expertise, you can avoid clawbacks and focus on growing your business. Final Thoughts The clawback of Qualifying Group Relief is an important part of UAE corporate tax law. While the relief helps businesses transfer assets without immediate tax, the conditions must be followed carefully to avoid problems later. With proper planning and professional advice, businesses can use this relief to their advantage without worrying about clawbacks. Contact Elite Auditing today to ensure your company stays compliant and tax efficient. FAQs Does clawback apply after two years? No, if all conditions are followed for two years, the clawback usually doesn’t apply. Can free zone companies use Qualifying Group Relief? Yes, but they must meet all conditions. If they don’t, the clawback applies. Can I appeal a clawback? Clawbacks are strictly enforced, but consulting the FTA or tax experts may help in unique cases.

In the UAE, businesses must understand corporate tax rules, especially if they operate as unincorporated partnerships. Under the UAE Corporate Tax Law, these partnerships have unique tax requirements that affect how income is taxed and reported. This guide, created by Elite Auditing, simplifies calculating taxable income for unincorporated partnerships. Whether you’re a small business owner or part of a professional collaboration, this article will help you understand the rules, requirements, and steps involved. What Is an Unincorporated Partnership? An unincorporated partnership is a business owned by two or more people or entities. These partners share profits, losses, and responsibilities based on their agreement. Unlike a company, an unincorporated partnership does not have a separate legal identity. Instead, the business and its partners are treated as one for legal and tax purposes. Common examples of unincorporated partnerships in the UAE include: Law firms Family-run businesses Small consultancy firms How UAE Corporate Tax Applies to Unincorporated Partnerships The UAE Corporate Tax Law has specific rules for unincorporated partnerships: Not Taxed as a Business: The partnership itself is not taxed. Instead, the partners pay tax on their share of the business income. Taxable Income for Partners: Each partner’s share of income is added to their taxable income. Partners are responsible for reporting and paying tax on their portion. This ensures that profits are taxed fairly, based on each partner’s share. Requirements for Calculating Taxable Income To calculate taxable income for an unincorporated partnership, you need to meet these key requirements: 1. Partnership Agreement A partnership agreement outlines how profits and expenses are shared among partners. This document is critical because it guides tax calculations. 2. Financial Records The partnership must keep detailed financial records, including: Income from sales or services Business expenses (e.g., salaries, rent, utilities) Each partner’s share of profits Accurate records ensure compliance with UAE tax laws. 3. FTA Registration The partnership and its partners must register with the Federal Tax Authority (FTA) if they engage in taxable activities. Also read: All About the Conditions to Qualify for Business Restructuring Relief Under UAE Corporate Tax How to Calculate Taxable Income for an Unincorporated Partnership Follow these steps to determine the taxable income: Step 1: Calculate the Partnership’s Net Income Net income is the total income from the business minus allowable expenses. Allowable expenses include costs like salaries, rent, and business utilities. Step 2: Divide the Income Among Partners Use the partnership agreement to split the net income among partners. Each partner gets their share based on the agreed percentages. Step 3: Report Income to the FTA Each partner reports their share of the partnership’s income to the FTA. Partners may deduct their own expenses or apply tax credits if eligible. Step 4: Pay Corporate Tax (If Applicable) If a partner’s taxable income exceeds certain thresholds, they may need to pay corporate tax. Common Scenarios in UAE Corporate Tax 1. Foreign Partners If a partnership includes foreign partners: Their tax obligations depend on both UAE laws and the tax laws in their home country. The UAE may offer relief to avoid double taxation if a treaty exists. 2. Small Business Relief Small partnerships with low income might qualify for small business relief, reducing their tax burden. 3. Capital Contributions and Withdrawals Contributions to the partnership by partners are not taxed. Withdrawals may have tax consequences, depending on the situation. Practical Tips for Partnerships 1. Create a Clear Agreement Make sure your partnership agreement specifies how income, expenses, and taxes are shared among partners. Update it as needed to reflect changes in the partnership. 2. Keep Accurate Records Detailed financial records are essential. Use professional accounting services to ensure compliance. 3. Plan for Tax Payments Partners should save money to cover their tax obligations. Planning ahead avoids surprises. 4. Stay Informed Tax laws in the UAE are evolving. Keep up to date with changes to ensure compliance. 5. Seek Professional Advice Working with experts like Elite Auditing ensures you understand and meet all tax requirements. Final Thoughts Unincorporated partnerships offer flexibility but require careful handling of tax obligations. Each partner must understand how their share of income is taxed and what steps to take for compliance. At Elite Auditing, we specialize in helping businesses like yours navigate UAE Corporate Tax rules. From financial records to tax planning, we provide expert support to ensure your partnership operates smoothly and complies with the law. Contact us today for advice or assistance with your tax needs. Let’s work together to build a strong foundation for your business in the UAE. FAQs Is an unincorporated partnership taxed directly? No. The partnership itself is not taxed. Each partner pays tax on their share of the income. What happens if there is no partnership agreement? If there’s no agreement, the FTA may divide income and expenses equally among partners. This can lead to disputes or tax issues. Are all business expenses deductible? No. Only expenses directly related to the business are deductible. Personal or unrelated costs cannot be deducted. Do foreign partners pay UAE tax? Foreign partners’ tax obligations depend on UAE laws and their home country’s tax rules. Double taxation relief may apply in some cases.

Understanding VAT (Value Added Tax) is important for businesses in Dubai and across the UAE. It becomes even more crucial when dealing with manpower and visa services. These services are essential for businesses, but they have different VAT rules that can be confusing. This guide will explain: What manpower and visa services are. How VAT applies to them. How to handle VAT correctly for these services. We’ll use simple language and examples to make it easy to follow. What Are Manpower and Visa Services? Manpower Services Manpower services are about providing workers to another business. For example: A construction company may hire workers from a manpower supplier. The workers remain employees of the supplier, not the hiring company. The supplier handles salaries, medical tests, and other requirements. The hiring company pays the supplier a fee for using these workers. Visa Services Visa services help companies get employment visas for their staff or assist individuals with visa applications. This can include: Preparing documents. Arranging medical tests. Applying for Emirates IDs. These services may be provided by a visa facilitator company or handled internally by businesses. Also read: How Does UAE’s VAT Impact Business Finances? How Does VAT Apply to These Services? Manpower Services Manpower services are always taxable under UAE VAT. The supplier must: Charge VAT at 5% on the service fee. Include this VAT in their tax returns. Example:If a company provides manpower services for AED 50,000: VAT at 5% = AED 2,500 Total = AED 52,500 Visa Services The VAT treatment for visa services depends on how they are charged: Service Fee: If the company charges a fee for helping with visas, this is a taxable service. VAT applies at 5%. Reimbursement: If the company only recovers the actual visa costs (like government fees) without adding extra charges, VAT does not apply. The Federal Tax Authority (FTA) provides guidance on this in Public Clarification VATP038. Key Differences Between Manpower and Visa Services Here’s a simple comparison: Aspect Manpower Services Visa Services What it involves Providing workers. Assisting with visa applications. Who benefits? The hiring company. The employee or employer. VAT treatment Always taxable (5%). Taxable if it includes a service fee. Examples Construction workers, hospitality staff. Employment visas, dependent visas. Steps to Ensure VAT Compliance Manpower Services Register for VAT: Businesses earning more than AED 375,000 annually must register for VAT. Charge VAT Correctly: Add 5% VAT to your service fees. Issue Proper Invoices: Show the VAT amount clearly on invoices. Visa Services Separate Charges: Clearly show service fees and reimbursement costs separately. Apply VAT Where Needed: Charge VAT on service fees but not on reimbursed visa costs. Keep Records: Maintain all receipts, invoices, and supporting documents. Common Examples and Calculations Manpower Services Example A company supplies 5 workers to a client for AED 40,000 per month. Fee: AED 40,000 VAT (5%): AED 2,000 Total: AED 42,000 The supplier must include AED 2,000 in their VAT return. Visa Services Example A visa facilitator charges AED 3,000 for processing an employment visa, including AED 2,500 as government fees and AED 500 as a service fee. Government Fees: AED 2,500 (no VAT). Service Fee: AED 500 (VAT at 5% = AED 25). Total: AED 3,025 Only the service fee is taxable. Tips for UAE Businesses Review FTA Guidance: Read Public Clarification VATP038 to understand how visa services are treated. Use Clear Invoices: Make it easy for your clients to see the VAT amount. Train Your Team: Educate staff on how VAT applies to these services. Work with Experts: Hire firms like Elite Auditing to ensure compliance. Stay Updated: VAT rules can change. Regularly check for updates from the FTA. Why Proper VAT Handling Matters If you don’t follow the VAT rules, your business may face: Fines from the FTA. Delays in processing your VAT returns. Loss of trust with clients. By understanding how VAT works for manpower and visa services, you can avoid these issues and focus on growing your business. Conclusion Manpower and visa services are essential for businesses in the UAE. Knowing how VAT applies to them helps you: Stay compliant. Avoid penalties. Build trust with clients and the authorities. At Elite Auditing, we specialize in VAT compliance, accounting, and tax services. Contact us to make your VAT processes easier and stress-free. FAQs Do businesses in a tax group need to charge VAT for manpower transfers? No. If the businesses are part of the same tax group, VAT does not apply to manpower transfers between them. Are visas for business travelers taxable? No, if you’re only reimbursing the actual visa cost. However, facilitation fees for arranging the visas are taxable. Can VAT on manpower and visa services be claimed back? Yes, businesses can reclaim VAT if these services are used for taxable activities.

Business restructuring can be complicated. However, the UAE Corporate Tax (CT) regime offers business restructuring relief to make the process easier for businesses. This relief allows companies to transfer assets, liabilities, or ownership during restructuring without immediate tax costs. In this article, Elite Auditing, your trusted tax and business partner in Dubai, explains the conditions and steps required to qualify for this relief. We’ll keep it simple, clear, and easy to follow. What Is Business Restructuring Relief? Business restructuring relief is a provision under UAE tax law. It allows businesses to reorganize without having to pay taxes immediately on transactions. This relief is helpful for companies merging, transferring ownership, or making changes to improve their operations. It encourages growth and efficiency while ensuring tax compliance. Why Is Business Restructuring Relief Important? Avoid Immediate Taxes: You don’t pay taxes right away on the transfer of assets or ownership. Encourages Growth: Restructuring becomes easier, allowing businesses to expand or adapt. Saves Money: Reduces financial strain during changes. Supports Compliance: Ensures businesses follow UAE tax rules. Conditions to Qualify for Business Restructuring Relief To qualify for this relief, businesses need to meet specific conditions set by the Federal Tax Authority (FTA). Below are the key requirements explained in simple terms. 1. Follow UAE Laws The restructuring process must comply with UAE regulations. For example: If two companies merge, they must follow the rules in the Commercial Companies Law (Articles 285–293). This ensures the process is legal and transparent. 2. Transferor and Transferee Must Be Taxable Persons Transferor: The person or business transferring assets or ownership. Transferee: The person or business receiving them. Both parties must: Be taxable under UAE Corporate Tax law. Be residents of the UAE or non-residents with a permanent establishment in the country. 3. Not Exempt or Qualifying Free Zone Persons The transferor and transferee should not be: Exempt persons. Qualifying free zone persons (e.g., businesses in free zones with special tax treatment). However, if either party becomes exempt or qualifying free zone persons after restructuring, they may still qualify for relief. 4. Same Financial Year-End Dates Both parties must have financial years ending on the same date. If they don’t: They must apply to the FTA to align their financial year-end dates. This ensures consistency in reporting and tax compliance. 5. Use the Same Accounting Standards Both businesses must follow the same accounting rules. For example: Most companies in the UAE use International Financial Reporting Standards (IFRS). Smaller businesses with revenue under AED 50 million may use IFRS for SMEs. If one uses IFRS and the other uses IFRS for SMEs, they must align their standards. 6. Valid Commercial Reasons for Restructuring The restructuring must have a genuine business purpose. It should not be done just to avoid taxes. Examples of valid reasons include: Improving efficiency. Preparing for expansion. Reducing costs. Types of Restructuring That May Qualify Here are examples of restructuring transactions that may qualify for relief: 1. Intra-Group Transfers Transferring assets or liabilities between companies in the same group. 2. Mergers and Acquisitions Combining two or more businesses into one entity. 3. Spin-offs or Divestments Splitting part of a business into a separate entity. 4. Asset Transfers Moving ownership of property, equipment, or intellectual property from one business to another. Steps to Apply for Business Restructuring Relief Qualifying for relief involves the following steps: Step 1: Check Eligibility Ensure your business meets all the conditions, such as: Both parties being taxable persons. Matching financial years and accounting standards. Step 2: Gather Documents Prepare the necessary paperwork, including: Financial statements. Contracts and agreements. Evidence of commercial reasons for restructuring. Step 3: Notify the FTA Inform the Federal Tax Authority (FTA) about your restructuring plans. Step 4: Submit an Application Send the application to the FTA along with supporting documents. Step 5: Wait for Approval The FTA will review your application and decide if relief can be granted. Lets Explore: Why Accounting Services Matter for Your Small Business in Dubai, UAE What Happens If You Don’t Meet the Conditions? If the conditions are not met: The transaction may not qualify for relief. Any taxable gains from the restructuring may be taxed immediately. Also, if conditions are violated later, the FTA may use clawback provisions to reverse the relief granted earlier. Practical Tips for Success 1. Work with Experts Partner with professional firms like Elite Auditing to ensure compliance and smooth processing. 2. Stay Organized Keep all required documents ready, including contracts, financial statements, and approvals. 3. Plan Ahead Restructuring takes time. Start early to meet all legal and tax requirements. 4. Monitor Tax Law Changes Stay updated on new rules or amendments to the UAE Corporate Tax Law. Conclusion Business restructuring relief is an excellent way to reorganize without immediate tax burdens. However, it requires careful planning and compliance with the UAE Corporate Tax Law. At Elite Auditing, we help businesses in Dubai and across the UAE navigate complex tax requirements. Whether you’re restructuring, expanding, or planning your next move, we’re here to guide you every step of the way. FAQs About Business Restructuring Relief Can free zone companies qualify for relief? Yes, but they must not be classified as qualifying free zone persons. Is there a time limit to align financial years? Yes, you must apply to the FTA within six months of the original financial year-end. Do we need professional help to apply for relief? While it’s not mandatory, working with tax experts ensures you meet all conditions and avoid mistakes. Will restructuring gains be taxed in the future? Yes, if the FTA finds that conditions were violated, relief may be withdrawn, and gains could be taxed later.

Running a small business is exciting but can also be tricky. Managing your finances is a big part of your success. In Dubai, where business laws and taxes are unique, having good accounting services is crucial. These services help you stay on top of your money and avoid problems. This article explains why accounting services are so important. It will show you what’s needed, how the process works, and answer common questions. Whether you’re new to business or want to grow, this guide is for you. What Do Accounting Services Include? Accounting services cover all the basics to help your business run smoothly. These include: BookkeepingKeeping track of daily sales, expenses, and payments. Financial ReportsSummarizing your income, cash flow, and overall financial health. Tax Filing (VAT)Making sure your tax returns are accurate and submitted on time. Budgeting and PlanningHelping you manage your money and plan. Audit SupportPreparing your business for financial audits to meet UAE laws. Why Accounting Is Essential for Small Businesses 1. Follow UAE Laws Dubai has strict business rules. Your business must: Keep accurate records for at least five years. File VAT (Value-Added Tax) returns on time. Be ready for audits, which are often required. Good accounting helps you avoid fines and keeps your business legal. 2. Manage Money Better Without tracking your finances, you might overspend or run out of cash. Accounting services help you: Track how much money is coming in and going out. Spot areas where you’re spending too much. Understand which products or services make the most profit. 3. Support Growth As your business grows, you’ll need better systems to handle more money and transactions. Accounting services help by: Creating financial reports to attract investors or get loans. Helping you plan and budget for expansion. Keeping your finances organized during growth spurts. How the Accounting Process Works Accounting might sound complicated, but it’s simple when broken down: Step 1: Record Transactions Keep a record of all sales, purchases, and expenses. This is the foundation of accounting. Use spreadsheets or accounting software for easy tracking. Step 2: Organize Records (Bookkeeping) Categorize and organize all your transactions. This helps create clear financial summaries. Step 3: Prepare Financial Reports Turn your records into financial statements like: Income Statement: Shows profit and loss. Cash Flow Statement: Tracks money coming in and going out. Balance Sheet: Gives a snapshot of your business’s financial position. Step 4: File Taxes (VAT) Submit VAT returns on time. This avoids penalties and ensures compliance with UAE tax rules. Step 5: Regular Updates Review your finances regularly with your accountant. This helps you stay on track and make better decisions. Common Challenges Small Businesses Face 1. Lack of Time Running a business takes a lot of energy. Managing your finances on top of everything else can feel overwhelming. Outsourcing accounting saves time. 2. Confusing Rules UAE tax and business rules, like VAT filing, can be hard to understand. A professional accountant knows these rules and ensures you follow them. 3. Cash Flow Problems Small businesses often struggle with having enough money to cover expenses. Accounting helps you plan and avoid shortages. 4. Mistakes in Records Errors in bookkeeping or VAT filings can lead to fines. Professional accountants make sure your records are accurate. Why Choose Elite Auditing? At Elite Auditing, we make accounting simple and stress-free for small businesses in Dubai. Here’s why clients trust us: 1. Expert Knowledge We understand UAE laws and make sure your business stays compliant. 2. Customized Services We know every business is different. Our services are tailored to meet your specific needs. 3. Modern Tools We use the latest accounting software to provide fast and accurate results. 4. Ongoing Support Our team is with you every step of the way—from bookkeeping to tax filing. Practical Tips for Small Business Owners Here are some tips to keep your finances on track: Stay Organized Keep all receipts, invoices, and transaction records in one place. This makes accounting easier. Use Accounting Software Tools like QuickBooks or Zoho Books make tracking your money simple. Hire Professionals An experienced accountant saves you time, prevents errors, and helps with tax compliance. Plan for Taxes Set aside money regularly to cover your VAT payments and avoid surprises. Conclusion Accounting services are vital for any small business in Dubai. They help you stay compliant with UAE laws, manage your finances, and plan for success. At Elite Auditing, we provide expert support tailored to your needs. From bookkeeping to VAT filing, we handle everything so you can focus on growing your business. Contact us today to learn how our services can make your small business thrive! FAQs Do I need accounting services for a small business? Yes! Proper accounting helps you manage money, avoid fines, and grow your business. How much do accounting services cost? Costs depend on your business size and needs. Elite Auditing offers affordable plans for small businesses. Can I do accounting myself? Yes, but it takes time and knowledge of UAE tax laws. A professional accountant makes the process faster and more accurate. What happens if I miss a VAT deadline? You may face heavy fines. Accounting services ensure you submit your returns on time. How can I improve my cash flow? Track your income and expenses regularly, cut unnecessary costs, and plan payments in advance.